US citizens living in the UK: the problems, pitfalls and planning opportunities

Share this article

With approximately quarter of a million US citizens living in the UK, we take a look at the problems, pitfalls and planning opportunities that their tax advisers must be aware of.

Key Points

What is the issue?

The United States has uniquely maintained a citizenship basis of taxation, meaning that US citizens, regardless of their residence, are fully liable to file and pay the US on worldwide income.

What does it mean to me?

Many are surprised to learn that, despite having never actually lived in the US themselves, or having left as a young child, they still have a full requirement to file and, in some cases, pay US taxes.

What can I take away?

If you are advising US citizens on their potential US tax obligations, double-check with your professional indemnity insurers to ensure it is covered, as some insurers exclude it as standard.

The ratification of the 16th Amendment to the United States constitution in 1913 imposed the first permanent income tax, and uniquely maintained a citizenship basis of taxation, meaning that US citizens, regardless of their residence, are fully liable to file and pay the US on worldwide income.

With approximately a quarter of a million US citizens living in the UK, tax advisers may inevitably come across American citizens, who may or may not be aware that they should be filing tax returns, and potentially paying tax, in the US.

Unexpected taxation

I recently received a hysterical phone call from an elderly lady who had moved to the UK from the US in 1974. She had just discovered, due to her bank applying the requirements of the US Foreign Account Tax Compliance Act (see below), that she should have been reporting her small pension to the IRS. She was terrified the IRS would be seeking extradition and that the police would shortly be breaking down her front door.

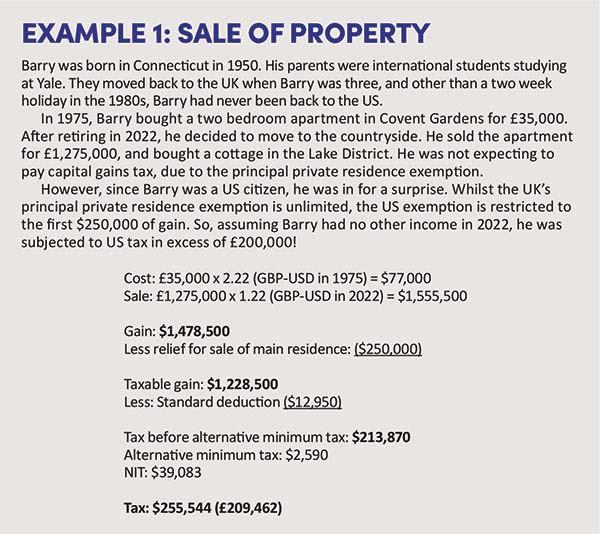

Further, it’s not only income and disposals of property (see Example 1: Sale of property) that must be reported. Since 1970, US Foreign Bank Account Reporting requirements mean that, subject to a de minimis of $10,000, the quantum of all non-US bank accounts must be reported too. If this $10,000 threshold is reached, all non-US bank accounts must be reported, even those with less than $10,000 in them. The $10,000 is calculated by adding up the highest balance, at any point in the year, of each foreign account.

The Foreign Bank Account Reporting is not reported to the IRS, but to the Financial Crimes Enforcement Network. Penalties for non-filing are high; up to $10,000 for a non-wilful non-filing. In the recent Supreme Court case of Bittner v United States (see bit.ly/3B3U8xP), Mr Bittner failed to report 272 bank accounts over a five year period. The IRS assessed a penalty of $2.72 million –$10,000 per unreported account! Mr Bittner challenged this, claiming that the $10,000 penalty should be per report, not per account. Fortunately, the Supreme Court agreed with him. We are currently in the process of appealing several wrongly imposed penalties.

The Foreign Account Tax Compliance Act

Since 2011, with the introduction of the Foreign Account Tax Compliance Act, a further asset reporting requirement has come into place. The reporting threshold is now satisfied only if the total value of the foreign financial assets is more than $200,000 on the last day of the tax year or more than $300,000 at any time during the tax year. These limits are doubled for married taxpayers filing jointly.

However, whilst Foreign Bank Account Reporting required reporting only of foreign bank accounts, the Foreign Account Tax Compliance Act requires more in-depth reporting, and also includes assets beyond accounts, such as stock ownership. Significantly, real estate does not need to be reported. The form is filed alongside the tax return.

As a result of a UK-US inter-governmental agreement, the Foreign Account Tax Compliance Act is now part of domestic UK law, by virtue of Finance Act 2013 s 222 and its supporting regulations. This means that UK banks need to establish whether their customers are US citizens and, if so, report their bank balances to the IRS via HMRC.

Who is an American?

The US operates with a combination of jus soli (whereby citizenship is acquired by birth within the territory of the state, regardless of parental citizenship) and jus sanguinis (whereby the nationality of children is the same as that of their parents, irrespective of their place of birth).

Almost anyone born in the US, regardless of his parent’s nationality or immigration status, is automatically a US citizen. (The exception is those born to a parent with diplomatic immunity.) Children of US citizens born abroad may also be automatic citizens, depending on how long their parents spent in the US prior to their birth.

Many are surprised to learn that, despite having never actually lived in the US themselves, or having left as a young child, they still have a full requirement to file and, in some cases, pay US taxes. Colloquially known as ‘Accidental Americans’, many traditionally applied the ‘ostrich algorithm’; by burying one’s head in the sand, the problem would somehow vanish of its own accord. Those who did try to slip back into the system would do so by means of a ‘quiet disclosure’ – i.e. by back-filing past tax returns without making a formal disclosure – and in the majority of cases, these were processed with no penalties or other repercussions.

Options for disclosure

Offshore Voluntary Disclosure Programs

This all changed in 2009, with the introduction of the first of four Offshore Voluntary Disclosure Programs, the last of which ended in 2018. Like the UK’s Liechtenstein Disclosure Facility (which gave eligible UK taxpayers the chance to declare their worldwide income and bring their UK tax affairs up to date quickly and without having to undergo an in depth investigation), these US schemes were intended to target individuals who had utilised foreign accounts to avoid tax. At least from the IRS’s perspective, they were highly successful, bringing in over $5.5 billion.

The main ‘selling point’ of the initiative was immunity from criminal prosecution. However, whilst penalties were reduced, they weren’t quashed entirely. And since the initiatives were intended to allow deliberate tax evaders to bring their affairs up to date, rather than penalise the Accidental Americans who were at no risk of criminal prosecution and in many cases had no tax to pay anyway, they were like using a sledgehammer to crack a nut.

The Streamlined Foreign Offshore Procedure

Thus, in 2012 (and significantly expanded in 2014), the Streamlined Foreign Offshore Procedure began, allowing Accidental Americans to become compliant with their US filing obligations without penalty.

The Streamlined Foreign Offshore Procedure is available to anyone who:

- satisfies the non-residency requirements (broadly, that for at least one of the previous three years, the individual did not have a US abode and was physically outside the United States for at least 330 full days);

- can certify that the non-filing was non-wilfull (i.e. due to negligence, inadvertence, mistake or conduct that is the result of a good faith misunderstanding of the requirements of the law); and

- either has unreported foreign taxable income or an unfiled Foreign Bank Account Report.

The Streamlined Foreign Offshore Procedure requires the filing of three delinquent tax returns, and six delinquent Foreign Bank Account Report.

If, for example, the Streamlined Foreign Offshore Procedure was filed on 1 June 2023, tax returns would need to be filed for 2019, 2020 and 2021, and Foreign Bank Account Reports for 2016 onwards, in addition to the 2022 tax return and report.

If the Streamlined Foreign Offshore Procedure was filed on 16 June 2023 (after the filing deadline for the 2022 return), tax returns would only need to be filed for 2020 onwards, and Foreign Bank Account Reports returns for 2017 onwards.

Other filing requirements

Two other filing requirements often catch people out.

Companies and Form 5471

US citizens who own a 10% or greater shareholding in UK companies need to file a Form 5471 attachment with the tax return (see bit.ly/42zhTtc). This is a highly complicated return, estimated by the IRS in 2015 as requiring 27 hours and 12 minutes to prepare, which excludes the 18 hours and 19 minutes estimated to learn about the form! (Since 2016, the IRS have ceased providing estimated time burdens, but the form has subsequently become even more complicated.)

Form 5471 requires reporting, amongst other things, the balance sheet and profit and loss of the company, under US Generally Accepted Accounting Principles (GAAP).

Controlled foreign companies

If the UK company is considered a controlled foreign company, tax may be due on certain passive income under what is known as Subpart F (and outside the scope of this article).

However in 2018, Congress, determined to avoid the indefinite deferral of tax of controlled foreign companies’ unremitted income, introduced a new liability – a tax on a pro-rata share of the foreign companies’ global intangible low-taxed income (GILTI).

Fortunately, there is an exemption in cases where the effective foreign tax rate is at least 90% of the US corporate tax rate. Since the US corporate tax rate is currently 21%, the effective rate to meet the high-tax exemption is 18.9%. This brings UK companies, with a headline corporation tax rate of 19%, within the scope the exception.

President Biden has indicated that he wishes to raise the US corporate rate to 28%, requiring a headline tax rate of 25.2% for an exemption. Even with the UK’s headline corporation tax rate increasing to 25%, this will not be sufficient to meet the exemption. However, the President alone cannot change tax rates; that requires agreement from both Houses of Congress.

Fiscal transparency

One possible option that may avoid these issues is to make an election for the UK company to be considered fiscally transparent. This entity classification election, colloquially known as a ‘check-the-box election’, enables the owner of the company to have the company’s income pass-through to the shareholders; equivalent to how the UK treats a limited liability partnership.

The company’s profits would thus be directly taxed on the shareholder as though they were self-employed, with the foreign tax credit allowing a set-off of UK corporation tax against US income tax. A totalisation agreement (the social security equivalent of a tax treaty) is in place between the US and the UK, avoiding the need to pay US Self-employment tax (the equivalent of Class 4 National Insurance).

However, with the company treated in the UK as a taxable entity, but in the US as fiscally transparent, this may trigger further complications due to the UK’s introduction of the hybrid mismatch legislation, introduced by Finance Act 2016. The UK Supreme Court case of George Anson v HMRC [2015] UKSC 44 illustrates some of the complications caused by hybrid and reverse hybrid entities.

In practice

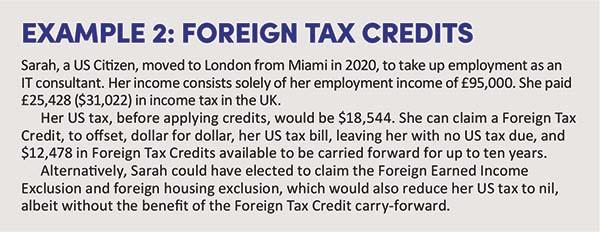

It’s not all bad news though. Whilst the US requires the filing of a tax return for anyone earning above a de minimis – currently $12,950 for an unmarried person under the age of 65 – in many cases, due to a combination of Foreign Tax Credits and other exemptions, there may be no US tax to pay. (See Example 2: Foreign Tax Credits).

Unlike the UK tax year which ends on 5 April, the US uses a calendar tax year ending on 31 December. Therefore, UK income will need to be apportioned to the correct US tax year. The tax return must be filed, and any tax due paid, by 15 June of the following year, although the filing date (but not the due date for payment) can be automatically extended until the 15 October if required, by filing Form 4868.

Another key difference between the US and UK’s tax system is that married couples can optionally file a joint return, including the income of both partners, but giving double allowances. This is the case even if one spouse is not a US citizen, as an election can be made for the non-citizen spouse to be considered a citizen for tax purposes (although this has no effect on immigration status).

This can be useful where one party is a non or low-paid earner, as income tax brackets are effectively doubled. (This is far more beneficial than the UK’s marriage allowance, and would avoid the need for artificial income splitting as seen in the Arctic Systems case of Jones v Garnett [2007] UKHL 35.) Further, children and other dependents can be ‘claimed’ on the return, providing significant tax benefits.

Pitfalls

Since UK marginal tax rates are generally higher than US rates, in the majority of cases, due to the pound for pound (or dollar for dollar) foreign tax credit available (see Example 2), in theory, no US should be due on UK income.

Problems arise, however, in cases where no UK tax is due. The most common examples are interest, dividends and gains arising in an ISA. Whilst these are tax-free in the UK, they are still taxable in the US, and a taxpayer with significant income from an ISA may not have enough foreign tax credits available to set off the US tax, creating a liability. (Conversely, certain investments that are tax-free in the US, such as municipal bonds, are fully taxable in the UK.) A particular concern is a share portfolio containing OEICs (open-ended investment companies), which are considered to be passive foreign investment companies (PFICs) and taxed at rates that can exceed 100%.

(A PFIC is a company that meets either or both of the following two criteria: (a) 75% of the company’s gross income comes from passive income; or (b) 50% of the company’s assets are held as investments. The asset gains are allocated pro-rata to each day in the holding period and aggregated within each tax year. Tax is then calculated at the highest marginal rate for that tax year, and interest calculated upon that. Generally, no foreign tax credit is allowed against the ‘prior year’ tax and interest charge. The lack of foreign tax credit and interest charges can push the effective tax rate on the gain to – in theory – above 100%.)

Gambling income is also taxable in the US. I once had a client inform me she had won £100,000 on a lottery. Sadly, this was fully taxable in the US.

As discussed above, principal private residence relief is restricted to the first $250,000 of gains, although for a married couple filing jointly, this is doubled to $500,000.

Trusts are also an issue that creates problems. Since even the briefest glimpse into how the US treats UK trusts would require this magazine to double in size, I will summarise in one word: ‘Beware!’

Time for some good news!

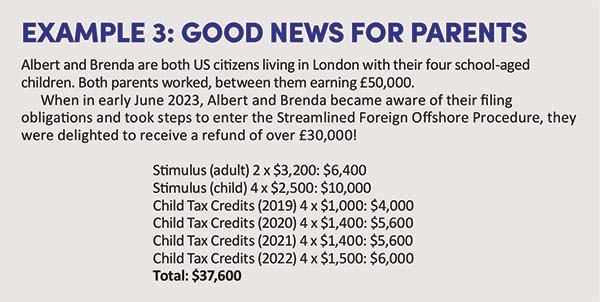

Every cloud has a silver lining. In some cases, taxpayers may end up with a refund. One significant benefit is the child tax credit, which is available to many US citizens with children worldwide, and dependant on income can be up to $1,500 per child under the age of 17 per year.

In response to Coronavirus, the US government paid three ‘stimulus checks’ to US citizens worldwide. Together, the three payments totalled $3,200 for adults, and $2,500 for children. Those who haven’t filed tax returns are not too late; it is still possible to claim as long as the relevant tax returns are filed by 15 June 2024. (See Example 3: Good news for parents.)

It is my understanding that the ‘stimulus checks’ are not taxable in the UK (see bit.ly/42EqquO).

A few final points

If you are advising US citizens on their potential US tax obligations, it would be a good idea to double-check with your professional indemnity insurers, to ensure it is covered, as some insurers exclude it as standard.

Advisors should be aware of their anti-money laundering requirements, which require a suspicious activity report to be made to the UK's National Crime Agency if they suspect a client of evading US tax.

I haven’t touched upon state tax, as it is usually (but not always) less relevant to expatriates, but in some circumstances may also need to be considered.

© Getty images/iStockphoto

Share this article